In South Africa, the challenging environment in which businesses are currently operating is widely recognised and covered by our news outlets. The features of this challenging operating business environment include, amongst other things, the confluence of load shedding, high inflation, high interest rates, sharp increases in electricity prices, foreign exchange volatility, ongoing geopolitical tensions, the erosion of foreign investment confidence in the country, as well as concerning levels of crime and corruption. All of these features, compounded together, have created what is probably the most difficult business environment I have experienced in my working career. The current economic environment is troubling; the disruption in business operations directly impacts consumers and runs the risk of increased social instability, due to the undoing of livelihoods and rise in poverty levels. With low levels of expected economic growth – combined with the breakdown of state infrastructure relating to energy, transport and logistics, and the slow pace of economic reforms to date – the urgency to address these issues cannot be overstated.

Against this backdrop, it is pleasing to note the Group’s ability to maintain positive earnings momentum. We are also proud of our teams’ successful completion of the Mediclinic Group Limited (Mediclinic) and Distell Group Holdings Limited (Distell)/Heineken International B.V. (Heineken) corporate transactions (1), both of which were implemented during the year under review. Both transformative transactions have been in the making for many years, and we are pleased to finally report on their successful completion.

The finalisation of these two transactions marks another inflection point in Remgro’s rich history. Prior to their implementation, approximately 70% of Remgro’s portfolio could be accessed directly via relevant issuers on various stock exchanges. The ratio between the value of the unlisted and listed portion of our portfolio has completely switched; the value of the unlisted portion of Remgro’s portfolio now sits at approximately 70%. This has materially increased Remgro’s scarcity factor, thereby positioning it for further growth.

We are also pleased with the progress we’ve made in delivering our other strategic priorities during the period. These priorities remain unchanged and we remain committed to consistently growing our triple bottom line, which includes unlocking value for our shareholders, efficient capital allocation and continued focus on our sustainability drive.

As an investment holding company, our number one priority is to unlock the intrinsic value of our assets. In pursuit of this, the following strategic actions were implemented to ensure we achieve growth in our core assets. These actions include, inter alia:

With the shift in the composition of Remgro’s portfolio, we remain committed to unlocking further value through an intensified focus on driving turnaround and growth in our core and growth assets, including Mediclinic, Heineken Beverages, Community Investment Ventures Holdings Proprietary Limited (CIVH), RCL Foods Limited (RCL Foods) and Siqalo Foods Proprietary Limited (Siqalo Foods).

The efficient allocation of capital is an intrinsic part of our strategy. We seek to deploy capital into our growth assets, and to maintain our cash-generating assets as feeders of our dividend payout capacity and capital for growth.

As further detailed in the Significant investment activities section, our capital allocation decisions during this reporting period included further investment into Mediclinic and Heineken Beverages with a focus on future growth, the sale of FirstRand Limited (FirstRand) shares, and the implementation of a R1 billion share repurchase programme, as we seek to unlock value for shareholders where Remgro’s share price trades at elevated discount levels compared to its intrinsic net asset value.

We continue to make progress on our Environmental, Social and Governance (ESG) journey. Our ambitions regarding sustainability are anchored in our long-held view of our social, environmental, and governance responsibility as a values-led business. In line with our intention to take a leading role in the development of ESG and corporate sustainability within a South African context, we’ve taken deliberate steps to progress our ESG journey.

In line with our commitment towards social and environmental sustainability, we are pleased to report on the appointment of a full-time sustainability and ESG expert, Ms Tanis Brown, to drive our ESG strategy across the Remgro Group, and partnering with the investee companies within our portfolio in driving this effort. Ms Brown has extensive knowledge and experience within the ESG field and will fulfil an important role in the next phase of Remgro’s ESG journey. Our immediate priorities include the following: further enhancing our measurement of, and reporting on, ESG related matters, as well as the continued implementation of the Remgro ESG strategy across the portfolio of businesses.

As a Group, and as a responsible corporate citizen, we have made some headway in embedding ESG into our business strategy, as well as partnering with our investee companies to improve and consistently integrate ESG practices and processes throughout our entire value chain.

A key part of our sustainability journey is reporting on our ESG progress and disclosures. It gives me great pleasure to report that we’ve honoured the commitment we made last year to include our first set of ESG disclosures aligned to the Task Force on Climate-Related Financial Disclosures (TCFD).

We remain unwavering in our commitment to unlocking sustainable stakeholder value and seek to maintain a disciplined approach, towards capital allocation, in pursuit of this ambition. We look to balance further investment into growth with maintaining an appropriate cash buffer and returning cash to shareholders in the form of dividends and share repurchases as and when appropriate.

Additional value unlock can be achieved through an intensified focus on our core turnaround and growth assets as well as the disposal of non-core assets, combined with a renewed focus on identifying attractive growth opportunities. We will also continue to embed sustainability, when considering new attractive growth opportunities, and work towards further improving our disclosures and shareholder engagement.

The proposed transaction between Vodacom Proprietary Limited (Vodacom) and CIVH(1) remains a priority for Remgro. We, together with CIVH and Vodacom management, fundamentally believe in the value of this transaction and remain committed towards unlocking value for our shareholders, which the achievement of approval from the relevant Competition Authorities would present. We remain confident that the positive social impacts of the proposed transaction on critical issues such as the democratisation of the internet in lower income areas; greater access to cheaper fibre to the greater South Africa; as well as the potential for job creation, and broader growth of the economy will be favourably considered by the Competition Tribunal of South Africa.

On 26 September 2022, the Mediclinic shareholders voted in favour of a cash offer by Manta Bidco Limited (Bidco), a newly formed company which is jointly owned by Remgro and MSC, to acquire the entire issued and to be issued ordinary share capital of Mediclinic, other than the Mediclinic shares Remgro already owned (the Mediclinic acquisition). The last conditions precedent in respect of the Mediclinic acquisition were met during May 2023 and on 6 June 2023, Mediclinic shareholders received 501 pence per Mediclinic share, being the offer price of 504 pence per Mediclinic share less the dividend of 3 pence per Mediclinic share that was paid on 26 August 2022. To enable the Mediclinic acquisition, Remgro sold its existing 328 497 888 Mediclinic shares (representing an interest of 44.6%) to Bidco in exchange for shares in Bidco and subscribed for further shares in Bidco amounting to £221 million (representing an additional indirect interest in Mediclinic of 5.4% and approximately 50% of Bidco’s transaction costs). MSC also subscribed for shares in Bidco amounting to £1 867 million (representing an indirect interest in Mediclinic of 50% and 50% of Bidco’s transaction costs).

On 15 February 2022, the Distell shareholders approved the combination of the Heineken Southern African business, including an interest in Namibia Breweries Limited, with the bulk of the Distell business (consisting of its cider, other RTDs (ready-to-drink) and spirits and wine business) in Heineken Beverages, a new unlisted entity controlled by Heineken. The transaction included the unbundling by Distell of the unlisted shares in Distell’s subsidiary, Capevin Holdings Proprietary Limited (Capevin), which holds Distell’s remaining assets, including its Scotch whisky business. The transaction, which was implemented on 26 April 2023, also included an offer by Heineken Beverages to Distell shareholders to acquire their Distell shares for R165 per share and/or unlisted shares in Heineken Beverages, or a combination thereof (subject to a potential scaling back of the issue of Heineken Beverages shares to Distell shareholders, electing to receive Heineken Beverages shares, to ensure a 65% shareholding by Heineken in Heineken Beverages), and an offer by Heineken to Distell shareholders to acquire their Capevin shares for R15 per share.

Remgro elected to receive Heineken Beverages shares for its Distell shares. However, as a result of the scale back, Remgro sold 7 607 803 Distell shares to Heineken Beverages on 26 April 2023 for R1 255 million (being R165 per Distell share) and exchanged the remaining 62 242 453 Distell shares for 62 242 453 Heineken Beverages shares (representing an interest of 15.5%). Following the implementation of the transaction, Remgro acquired a further 13 218 475 shares in Heineken Beverages for R2 181 million (or R165 per share excluding transaction costs), in a series of off-market transactions. These transactions increased Remgro’s interest in Heineken Beverages to 18.8%. The next year’s focus will be on integration of these businesses.

Remgro did not accept the cash offer made by Heineken for the Capevin shares and, as a result, Remgro’s shareholding in Capevin mirrors the shareholding that was previously held in Distell, being an economic interest of 31.4% and a voting interest of 55.9%.

As previously reported, Vodacom will, through a combination of assets of approximately R4.2 billion and cash of at least R6.0 billion, acquire up to 40% of the ordinary shares of a newly created wholly owned subsidiary of CIVH (namely Maziv Proprietary Limited (Maziv)). Maziv holds inter alia CIVH’s current interests in Vumatel and DFA. As a result of the proposed transaction, Remgro’s indirect interest in DFA and Vumatel will dilute with the entrance of Vodacom as a shareholder, however Remgro will also obtain an indirect interest in the assets contributed by Vodacom. During August 2023, The Competition Commission South Africa announced its non-binding recommendation to the Competition Tribunal to prohibit the proposed transaction. Remgro and CIVH remain committed to the proposed transaction and firmly believe that, should the implementation of the proposed transaction ultimately be permitted by the Competition Tribunal, it will deliver significant benefits to South African consumers and the broader economy.

On 17 October 2022 Remgro unbundled its investment in Grindrod to its shareholders as a dividend in specie amounting to R1 640 million, in the ratio of 30.70841 Grindrod shares for every 100 Remgro shares held.

During July 2022 Remgro sold 19.2 million FirstRand shares for R959 million (being R49.945 per FirstRand share). These FirstRand shares were part of the 60 million FirstRand shares that were hedged through a series of options, which became exercisable during June and July 2022. Remgro sold the 60 million FirstRand hedged shares to net settle the option liabilities. The other 40.8 million FirstRand shares were sold during June 2022.

Pursuant to a general share repurchase programme of R1 billion, Remgro, through a wholly owned subsidiary, acquired 6 583 676 Remgro ordinary shares in the open market between 19 June 2023 and 2 August 2023 (Remgro repurchased shares). These shares represent 1.2% of the Company’s issued ordinary shares immediately prior to the repurchase. At 30 June 2023, 1 882 333 Remgro repurchased shares had been acquired at an average price of R145.62 per share for a total amount of R274 million. Subsequent to 30 June 2023, another 4 701 343 Remgro repurchased shares were acquired at an average price of R154.40 per share for a total amount of R726 million. The share repurchase programme was completed on 2 August 2023. These Remgro repurchased shares were acquired as part of an ongoing strategic focus on returning value to shareholders through a disciplined capital allocation plan.

The following tables represent the cash effects of Remgro’s investment activities for the year to 30 June 2023. These activities exclude the investing activities of Remgro’s operating subsidiaries, i.e. RCL Foods Limited, Siqalo Foods Proprietary Limited, Wispeco Holdings Proprietary Limited and Capevin Holdings Proprietary Limited.

| Investments made and loans granted | R million |

|---|---|

| Mediclinic (including costs) | 4 538 |

| Heineken Beverages (including scale back and costs) | 1 062 |

| Asia Partners (offshore) | 159 |

| Invenfin Proprietary Limited | 75 |

| Pembani Remgro Infrastructure Fund (PRIF) | 57 |

| Other | 44 |

| 5 935 | |

| Investments sold and loans repaid | R million |

|---|---|

| FirstRand | 1 199 |

| Milestone Capital Funds (offshore) | 135 |

| PRIF | 127 |

| Milestone Capital Investment Holdings Limited (offshore) | 89 |

| Other | 43 |

| 1 593 | |

The table below summarises the investment commitments of Remgro as at 30 June 2023

| Investment commitments | R million |

|---|---|

| PRIF | 1 536 |

| Asia Partners (offshore) | 886 |

| Other | 14 |

| 2 436 | |

As in my previous reports, this section serves to provide insight into Remgro’s valuation methodology and the integrity thereof; to assist stakeholders with understanding Remgro’s intrinsic net asset value, which we believe remains the most appropriate indicator of the value added to the benefit of our shareholders.

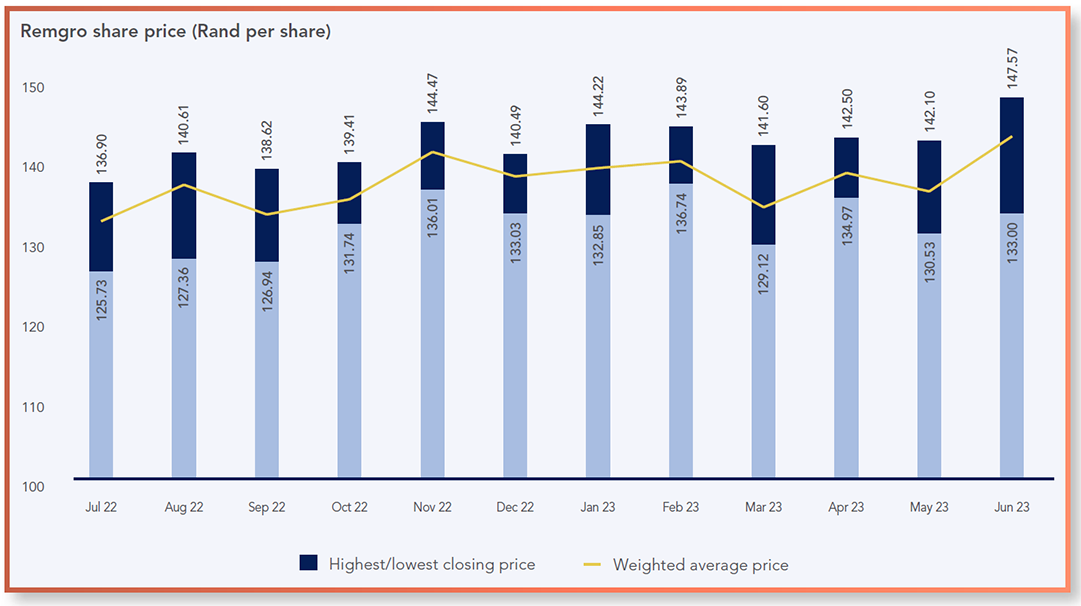

Remgro’s intrinsic net asset value per share increased by 16.6% from R213.10 at 30 June 2022 to R248.47 at 30 June 2023. The closing share price at 30 June 2023 was R147.05 (2022: R129.91), representing a discount of 40.8% (2022: 39.0%) to the intrinsic net asset value. As at 30 June 2023, 72% of the value of Remgro’s investment portfolio were represented by unlisted investments (2022: 33%). In this regard, it is worth noting that prior to the recently completed corporate transactions relating to Remgro’s investments in Mediclinic and Distell, as well as the unbundling of Remgro’s interest in RMB Holdings Limited (RMH) on 8 June 2020, 23% of the value of Remgro’s investment portfolio were represented by unlisted investments, with the share price trading at a discount to intrinsic net asset value of less than 30%. While the subsequent widening of the discount was not anticipated at the time, it does highlight the importance of demonstrating the veracity of the intrinsic net asset valuations in a portfolio that has pivoted towards more unlisted investments.

The intrinsic net asset value of the Group includes valuations of all investments, incorporating subsidiaries, associates, and joint ventures, either at listed market value or, in the case of unlisted investments, other inputs for the assets that are not based on observable market data.

Guidance in completing the valuations is obtained from IFRS 13: Fair Value Measurement, where Fair Value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. A fair value measurement assumes that a hypothetical transaction to sell an asset takes place in the principal market or, in its absence, the most advantageous market for the asset.

The values derived from the valuation exercise performed at measurement date fall within the IFRS 13 framework which requires, in the context of discounted cash flow valuations, the equity beta, capital structure and cost of debt be determined based on information obtained for similar assets or market participants, after certain adjustments are made. This impacts the weighted average cost of capital (WACC) used when discounting the cash flows for purposes of the IFRS 13 valuation and is expected to be different from those applied in a transactional valuation approach, as the target or actual inputs are replaced with inputs derived from considering the position of hypothetical market participants. Consequently, a valuation derived by applying the IFRS 13 framework is expected to differ from a transactional valuation.

In ensuring the veracity of Remgro’s intrinsic net asset valuations, the Valuation Subcommittee assists the Audit and Risk Committee to:

The Valuation Subcommittee is chaired by Mr Fred Robertson and consists of five non-executive directors (being two directors who serve on the Audit and Risk Committee and three directors who serve on the Investment Committee), the Chief Executive Officer, and the Chief Financial Officer. This function has become increasingly important as Remgro’s portfolio has evolved towards more unlisted investments.

The table below compares the Remgro intrinsic net asset value per share with certain selected JSE indices at 30 June during the last five years. The material decrease in the Remgro share price and intrinsic net asset value on 30 June 2020 reflects the unbundling of Remgro’s interest in RMH on 8 June 2020, as well as the negative impact of the Covid-19 pandemic.

| 30 June 2023 |

30 June 2022 | 30 June 2021 | 30 June 2020 |

30 June 2019 |

|

|---|---|---|---|---|---|

| Intrinsic net asset value – Rand per share | 248.47 | 213.10 | 177.33 | 154.47 | 233.03 |

| JSE | |||||

| – All Share Index | 76 028 | 66 223 | 66 249 | 54 362 | 58 204 |

| – Capped Swix All Share Index | 21 039 | 19 371 | 18 865 | 15 184 | 17 685 |

| – Fin & Ind 30 Index | 103 116 | 81 092 | 83 912 | 70 975 | 77 459 |

| – Financial 15 Index | 16 057 | 14 686 | 13 103 | 10 034 | 16 993 |

| – Healthcare | 6 282 | 5 362 | 4 981 | 4 344 | 5 225 |

| Remgro share price (Rand) | 147.05 | 129.91 | 114.60 | 99.90 | 187.90 |

The following table compares Remgro’s IRR with that of certain selected JSE indices. For this purpose it has been

assumed that dividends, which include unbundlings such as Remgro’s interest in RMH, have been reinvested in either

Remgro shares or in the particular index, depending on the specific calculation.

| One year 30 June 2023 (% year on year) |

Three years 30 June 2023 (% compounded per annum) |

Period from 28 October 2008(1) to 30 June 2023 (% compounded per annum) |

|

|---|---|---|---|

| JSE – All Share Index |

19.6 | 16.1 | 13.6 |

| – Capped Swix All Share Index | 13.5 | 15.7 | n/a(2) |

| – Fin & Ind 30 Index | 31.1 | 16.0 | 15.5 |

| – Financial 15 Index | 15.6 | 21.7 | 12.3 |

| – Healthcare | 19.5 | 30.7 | 15.1 |

| Remgro share price | 17.1 | 15.6 | 11.4 |

| Intrinsic net asset value | 20.6 | 19.1 | 12.9 |

At the start of the second quarter of 2023, there was a fair amount of apprehension that, following a reasonable start to the year, real GDP in South Africa could be under severe pressure once again. In large part, the concern stemmed from the risk of intensified load shedding during the winter months. In the end, the intensity of load shedding eased in June. Along with a strong increase in private sector investment in machinery and equipment, this ensured another quarter of GDP expansion in the second quarter.

Despite the temporary reprieve in the constraint on production and the cost of keeping the lights on, the SA economy remains under significant pressure amid energy and logistical constraints, as well as rampant crime and corruption. In addition, the latest survey data (PMIs) suggests that domestic demand is taking strain amid restrictive borrowing costs and stubbornly elevated relative prices, mainly food. Although international expansion continued in the second quarter, global growth momentum seems to have slowed at the end of the quarter and the incoming data indicates mixed trends for economic activity in South Africa’s main trading partners. While US growth was surprisingly solid, China’s first quarter reopening bounce ran out of steam in the second quarter. Economic activity remains very subdued in the Eurozone. Looking forward, amid contracting money supply, a deeply inverted yield curve, and a multi-month decline in the leading indicator, the US is still expected to be in a mild recession from late 2023. Overall, the delayed impact, including on labour markets, of aggressive developed country policy interest rate increases, is expected to push world growth lower in 2024.

On the global inflation front, price pressures at the headline level continue to moderate as Covid-19 and Russia-Ukraine War effects unwind but remain well above central bank targets. Furthermore, especially in some developed countries, underlying (core) inflation is still stubbornly elevated and interest rates are set to remain higher for longer. Given this backdrop, the South African economy is unlikely to be boosted by a positive near-term global growth impulse. On the contrary, partly due to major non-gold domestic export commodity prices being under pressure, the global environment is moving from a tailwind during the last two years to a headwind for South Africa. Lower prices for key SA export commodities are already having adverse implications for South Africa’s fiscal ratios, which are tracking significantly worse than the National Treasury’s expectation in the February budget.

After contracting by a less-than-previously estimated 1.1% quarter-on-quarter in the fourth quarter of 2022, SA real GDP growth expanded by around 0.5% during both the first and the second quarters of 2023. Despite downside risks in the second half of the year, a decent first half suggests that the South African economy can grow by about 0.5% in real terms during 2023. The narrative of improved growth in 2024 remains largely unchanged. Global concerns notwithstanding, an easing in the domestic power constraint as more private sector-driven generation projects come on stream, combined with Eskom returning major units currently on long-term outages, should see SA real GDP growth accelerate to above 1% next year. If nothing else, the partial lifting of the energy constraints should support business, consumer, and investor confidence. In terms of the major demand-side GDP components, faster rates of private sector real fixed investment growth are projected to be the key driver of an improved GDP performance in 2024, and beyond.

The rate of increase for headline consumer inflation (CPI) in South Africa continued to moderate in recent months. Even so, as the rand hit new all-time lows against major currencies in May, the SA Reserve Bank (SARB) lifted the policy interest to the current level of 8.25% (prime rate at 11.75%). As food price increases continue to moderate, the outlook for inflation is reasonably constructive. Along with the elevated oil price, a sustained rand weakness provides the most pronounced upside risk to this view. Given an assumption that headline CPI will remain on a disinflationary path, and also because of South Africa’s growth struggles, the SARB kept the repo rate unchanged in July. The policy rate is now set to be on hold for a prolonged period until inflation moves closer to the SARB’s preferred 4.5% mark and/or the US central bank (Fed) starts to reduce its policy rate. At this stage, both events are likely to materialise in the first half of 2024.

The rand weakened by 9.5%, 12% and 16% respectively against the US dollar, the euro, and the UK pound in the first half of 2023. A worsening of domestic macro fundamentals, including the move from a current account surplus to a deficit, South Africa’s Greylisting by the Financial Action Task Force (FATF) in February, as well as a diplomatic tensions with the US, dented foreign investor sentiment. Buoyed by the load shedding reprieve in June, together with indications that the Fed has reached the end of its hiking cycle, the local currency briefly recovered from its weakest levels in May. At current levels, the rand remains undervalued against major currencies.

As noted in my introduction, the increasing risk of social unrest in South Africa is troubling. This was further amplified by the recent taxi industry strike in the Western Cape, which turned violent and resulted in the loss of lives. The importance of urgently dealing with both the socio-political and economic issues facing our country is paramount.

Amidst all the headwinds South Africa is currently facing, Remgro remains confident about the resilience of its portfolio.

I wish to thank my colleagues at Remgro and our underlying investee companies for another positive year, and I am grateful for our Board whose input and guidance remains invaluable.

I look forward to the year ahead as Remgro continues to strive towards being the trusted investment company of choice that consistently creates sustainable stakeholder value.

Jannie Durand

Chief Executive Officer

Stellenbosch

20 September 2023

Investment |

Valuation methodology |

|---|---|

| Mediclinic | Sum-of-the-parts (external valuation) |

| CIVH | Discounted cash flow method |

| Heineken Beverages | Price of recent investment |

| Siqalo Foods | Discounted cash flow method |

| Air Products | Discounted cash flow method |

| TotalEnergies | Discounted cash flow method |

| KTH | Sum-of-the-parts (external valuation) |

| Capevin | Sum-of-the-parts |

| Wispeco | Discounted cash flow method |

| Business Partners | Net asset value |

| Prescient China Equity Fund | Sum-of-the-parts |

| Milestone China Opportunities Fund III (Milestone III) | Sum-of-the-parts |

| SEACOM | Discounted cash flow method |

| eMedia Investments | Comparable market price |

| Asia Partners (Fund I & II) | Sum-of-the-parts |

| PRIF | Sum-of-the-parts |

| PGSI | Discounted cash flow method |

| 30 June 2023 | 30 June 2022 | |||

|---|---|---|---|---|

| R million | Book value | Intrinsic value(1) |

Book value |

Intrinsic value(1) |

| Healthcare | ||||

| Mediclinic | 41 050 | 47 268 | 26 681 | 29 568 |

| Consumer products | ||||

| Distell | 8 386 | 11 969 | ||

| Heineken Beverages(2) | 12 495 | 12 451 | ||

| Capevin(2) | 1 677 | 1 576 | ||

| RCL Foods(2) | 9 152 | 7 141 | 8 816 | 7 355 |

| Siqalo Foods(2) | 6 212 | 6 007 | 6 261 | 6 345 |

| Financial services | ||||

| OUTsurance Group | 5 764 | 15 957 | 5 307 | 13 069 |

| Business Partners(2) | 1 289 | 1 260 | 1 193 | 1 193 |

| Infrastructure | ||||

| CIVH | 7 025 | 14 300 | 6 905 | 13 756 |

| Grindrod | 1 559 | 1 559 | ||

| SEACOM | 98 | 796 | 40 | 776 |

| Other infrastructure investments | 57 | 57 | 67 | 67 |

| Industrial | ||||

| Air Products | 1 282 | 4 911 | 1 162 | 4 690 |

| TotalEnergies | 3 063 | 3 338 | 3 158 | 3 274 |

| Wispeco(2) | 1 619 | 1 330 | 1 448 | 1 402 |

| Other industrial investments | 204 | 320 | 189 | 379 |

| Diversified investment vehicles | ||||

| KTH | 1 878 | 2 370 | 1 497 | 2 145 |

| Prescient China Equity Fund | 1 137 | 1 137 | 1 189 | 1 189 |

| Invenfin | 771 | 1 136 | 804 | 1 050 |

| Other diversified investment vehicles | 1 760 | 1 760 | 1 864 | 1 864 |

| Media | ||||

| eMedia Investments(2) | 897 | 659 | 856 | 738 |

| Other media investments | 154 | 182 | 111 | 150 |

| Portfolio investments | ||||

| FirstRand(3) | 6 889 | 6 889 | 7 141 | 7 141 |

| Discovery | 6 167 | 6 167 | 5 410 | 5 410 |

| Momentum Metropolitan | 1 816 | 1 816 | 1 439 | 1 439 |

| Other portfolio investments | 769 | 769 | 809 | 809 |

| Social impact investments | 126 | 126 | 132 | 132 |

| Central treasury | ||||

| Cash at the centre(4) | 9 001 | 9 001 | 12 280 | 12 280 |

| Debt at the centre | (7 857) | (7 857) | (7 838) | (7 838) |

| Other net corporate assets | 1 425 | 2 122 | 1 577 | 2 221 |

| Intrinsic net asset value (INAV) | 115 920 | 142 989 | 98 443 | 124 132 |

| Potential CGT liability(5) | (4 186) | (3 930) | ||

| INAV after tax | 115 920 | 138 803 | 98 443 | 120 202 |

| Issued shares after deduction of shares repurchased (million) | 558.6 | 558.6 | 564.1 | 564.1 |

| INAV after tax per share (Rand) | 207.51 | 248.47 | 174.52 | 213.10 |

| Remgro share price (Rand) | 147.05 | 129.91 | ||

| Percentage discount to INAV | 40.8 | 39.0 | ||