| 1. | BASIS OF PREPARATION | ||||

|

The summary consolidated financial statements are prepared in accordance with the requirements of the JSE Limited (JSE) for summary financial statements, and the requirements of the Companies Act applicable to summary financial statements. The JSE requires summary financial statements to be prepared in accordance with the framework concepts and the measurement and recognition requirements of International Financial Reporting Standards (IFRS) and the SAICA Financial Reporting Guides as issued by the Accounting Practices Committee and Financial Pronouncements as issued by the Financial Reporting Standards Council and to also, as a minimum, contain the information required by IAS 34: Interim Financial Reporting. |

|||||

|

The accounting policies applied in the preparation of the consolidated financial statements from which the summary consolidated financial statements were derived are in terms of IFRS and are consistent with those accounting policies applied in the preparation of the previous consolidated annual financial statements, with the exception of the implementation of IFRIC 21: Levies and the amendments to IAS 19: Employee Benefits, IAS 32: Financial Instruments Presentation, IAS 36: Impairment of Assets and IAS 39: Financial Instruments Novation of derivatives and continuation of hedge accounting. The adoption of these interpretations and amendments had no impact on the results of either the current or prior year. The financial statements have been prepared under the supervision of the Chief Financial Officer, Leon Crouse CA(SA). |

|||||

|

The summary consolidated financial statements do not contain all the information and disclosures required in the consolidated financial statements. The summary consolidated financial statements have been extracted from the audited consolidated financial statements upon which PricewaterhouseCoopers Inc. has issued an unqualified report. The audited consolidated financial statements and the unqualified audit report are available for inspection at the registered office of the Company. |

|||||

| 2. | HEADLINE EARNINGS RECONCILIATION | ||||

| R million | 30 June 2015 | 30 June 2014 | |||

| Net profit for the year attributable to equity holders | 8 715 | 6 917 | |||

| Plus/(minus): | |||||

| Net impairment of equity accounted investments | 99 | (92) | |||

| Impairment of other investments | 79 | 80 | |||

| Net impairment of property, plant and equipment | 94 | (5) | |||

| Impairment of assets held for sale | 16 | – | |||

| Recycling of foreign currency translation reserves | – | (32) | |||

| (Profit)/loss on sale of equity accounted investments | (984) | 83 | |||

| (Profit)/loss on sale of other investments | 288 | (98) | |||

| Net surplus on disposal of property, plant and equipment | (5) | (12) | |||

| Non-headline earnings items included in equity accounted earnings of equity accounted investments | (231) | (244) | |||

| Net surplus on disposal of property, plant and equipment | (111) | (131) | |||

| Profit on the sale of investments | (271) | (174) | |||

| Net impairment of investments, assets and goodwill | 213 | 262 | |||

| Other non-recurring and capital items | (62) | (201) | |||

| Taxation effect of adjustments | (50) | 33 | |||

| Non-controlling interest | (25) | 5 | |||

| Headline earnings | 7 996 | 6 635 | |||

| 3. | EARNINGS AND DIVIDENDS | ||||

| Cents | 30 June 2015 | 30 June 2014 | |||

| Headline earnings per share | |||||

| – Basic | 1 555.0 | 1 292.4 | |||

| – Diluted | 1 541.8 | 1 270.3 | |||

| Earnings per share | |||||

| – Basic | 1 694.9 | 1 347.3 | |||

| – Diluted | 1 680.9 | 1 325.7 | |||

| Dividends per share | |||||

| Ordinary | 428.00 | 389.00 | |||

| – Interim | 169.00 | 156.00 | |||

| – Final | 259.00 | 233.00 | |||

| 4. | INVESTMENTS | ||||

| (Refer annexures A and B) | |||||

| R million | 30 June 2015 | 30 June 2014 | |||

| Listed investments | |||||

| Associated | |||||

| – Book value | 41 533 | 36 601 | |||

| – Market value | 97 926 | 79 734 | |||

| Other | |||||

| – Book value | 902 | 880 | |||

| – Market value | 902 | 880 | |||

| Unlisted investments | |||||

| Associated | |||||

| – Book value | 11 336 | 11 090 | |||

| – Directors valuation (unaudited) | 22 516 | 22 497 | |||

| Joint ventures | |||||

| – Book value | 4 962 | 4 478 | |||

| – Directors valuation (unaudited) | 13 295 | 11 063 | |||

| Other | |||||

| – Book value | 1 591 | 1 762 | |||

| – Directors valuation | 1 591 | 1 762 | |||

| 5. | ASSETS and liabilities HELD FOR SALE | ||||

|

During June 2015, Remgro entered into an agreement with funds managed by Cinven to acquire 119 923 335 Spire shares (equivalent to a 29.9% shareholding in Spire). In conjunction with the transaction, Remgro and Mediclinic concluded an agreement whereby Mediclinic would acquire Remgro’s interest in Spire, subject to a successful Mediclinic rights issue. Total assets and liabilities are |

(175) | – | |||

| Investment | 8 275 | – | |||

| Trade and other creditors | (8 276) | – | |||

| Derivative instruments | (174) | – | |||

| Various other assets and liabilities classified as held for sale | 242 | 568 | |||

| Assets | 259 | 754 | |||

| Liabilities | (17) | (186) | |||

| 67 | 568 | ||||

| R million | 30 June 2015 | 30 June 2014 | |||

| 6. | Additions to and replacement of property, plant and equipment | 853 | 852 | ||

| 7. | Capital and investment commitments | 5 847 | 1 105 | ||

|

(Including amounts authorised but not yet contracted for, including R4.1 billion in respect of the Mediclinic rights issue) |

|||||

| 8. | Guarantees and contingent liabilities | 316 | 306 | ||

| 9. | Dividends received from equity accounted investments set off against investments | 3 077 | 3 568 | ||

| 10. | EQUITY ACCOUNTED INVESTMENTS | ||||

| Share of after-tax profit of equity accounted investments | |||||

| Profit before taking into account impairments, non-recurring and capital items | 8 332 | 8 584 | |||

| Net impairment of investments, assets and goodwill | (213) | (262) | |||

| Profit on the sale of investments | 271 | 174 | |||

| Other non-recurring and capital items | 62 | 201 | |||

| Profit before tax and non-controlling interest | 8 452 | 8 697 | |||

| Taxation | (1 129) | (1 558) | |||

| Non-controlling interest | (95) | (286) | |||

| 7 228 | 6 853 | ||||

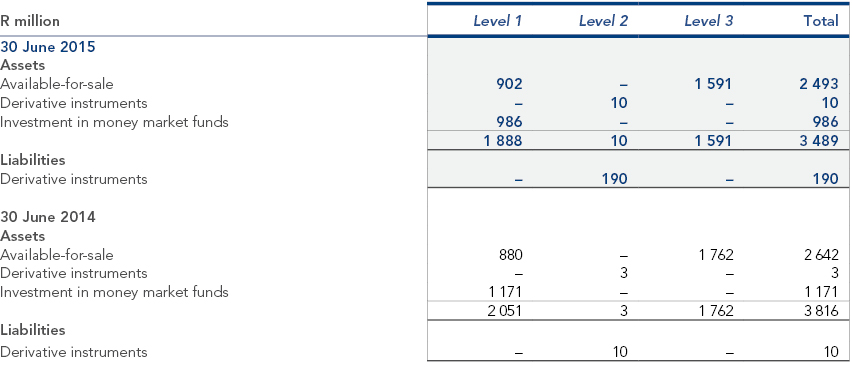

| 11. | Fair value remeasurements | ||||

| The following methods and assumptions are used to determine the fair value of each class of financial instruments: | |||||

|

Financial instruments available-for-sale and investment in money market funds: Fair value is based on quoted market prices or, in the case of unlisted instruments, appropriate valuation methodologies, being discounted cash flow, liquidation valuation or actual net asset value of the investment. |

|||||

|

Derivative instruments: The fair value of derivative instruments is determined by using mark-to-market valuations. |

|||||

|

Financial instruments measured at fair value are disclosed by level of the following fair value hierarchy: |

|||||

|

Level 1 Quoted prices (unadjusted) in active markets for identical assets or liabilities; |

|||||

|

Level 2 Inputs (other than quoted prices included within level 1) that are observable for the asset or liability, either directly (as prices) or indirectly (derived from prices); and |

|||||

|

Level 3 Inputs for the asset or liability that are not based on observable market data (unobservable inputs). |

|||||

|

The following table illustrates the fair values of financial assets and liabilities that are measured at fair value, by hierarchy level: |

|||||

|

|||||

|

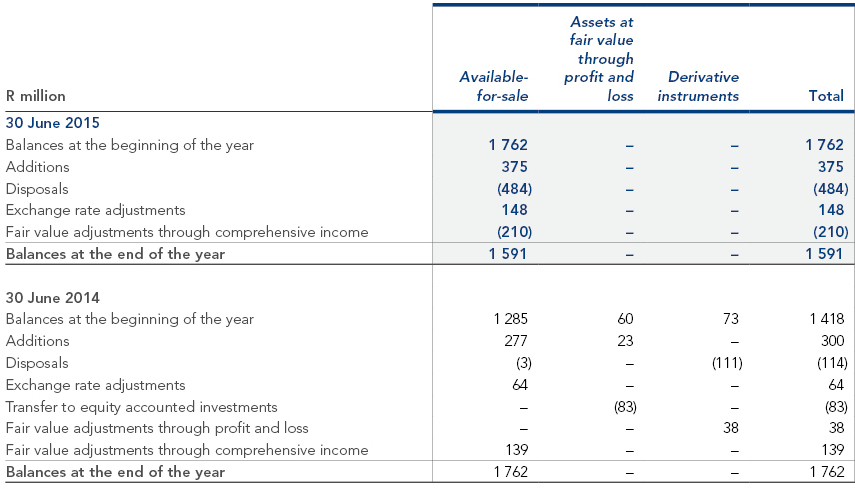

The following table illustrates the reconciliation of the carrying value of level 3 assets from the beginning to the end of the year: |

|||||

|

|||||

|

There were no transfers between the different levels. |

|||||

|

Level 3 investments consist mainly of investments in the Milestone China entities (Milestone), the Kagiso Infrastructure Empowerment Fund (KIEF) and the Pembani Remgro Infrastructure Fund (PRIF) amounting to R1 058 million, R322 million and R150 million respectively. These investments are all valued based on the fair value of each investments underlying assets, which are valued using a variety of valuation methodologies. Listed entities are valued at the last quoted share price on the reporting date, whereas unlisted entities methods include discounted cash flow valuations, appropriate earnings and revenue multiples. |

|||||

|

Milestone’s fair value consists of listed investments (42%), cash and cash equivalents (4%) and unlisted investments (54%). Two-thirds of the unlisted investments were acquired during the current financial year and were valued at cost as Milestones management considers the transaction price to be the fair value of the investments, while the remaining one-third was valued at approximately R190 million. KIEF’s investments were valued using the discounted cash flow method. PRIF’s main asset is the investment in ETG Group and it was valued using appropriate revenue and earnings multiples based on peer group companies to determine a price-to-book valuation. |

|||||

|

Changes in the valuation assumptions of the above unlisted investments will not have a significant impact on Remgro’s financial statements. |

|||||

- Overview of Business

- Reports to shareholders

- Governance and Sustainability

- Financial report